Every business owner is naturally curious about just how much their business is worth. However, for every business that sells at an attractive price, there are others that struggle to sell, let alone fetch a premium. The question is, what makes a difference?

When you come to sell a business the first question is, what are you selling? In most cases, this is fixtures and fittings, plant and

equipment, stock on hand, and the goodwill of the business. Generally, a buyer won’t want to purchase your liabilities or your business

structure, nor will they want to collect your outstanding debtors. Most business sales become a sale of business assets.

These assets are relatively easy to value with the exception of the goodwill. The value of plant and equipment and trading stock can

generally be agreed. The tension tends to be around the value of the goodwill because goodwill is made up of many intangible assets that

can’t be readily quantified.

We can all agree that there is value in these assets but the question is, how much? Goodwill is basically the value of the future free

cashflow of the business. Based on how your business is structured, it is the value of the profits the business can generate in the

future. This is what a buyer is prepared to pay for.

If a buyer has a reasonable certainty of profits and free cashflow in the future, then this is worth something. By comparison, a start-up

business will have a higher level of risk and no certainty that profits can be generated. In general, a new business may need to trade for a

number of years at a loss before it can establish itself and generate profits. Goodwill is what you are prepared to pay to avoid the

risk and the ‘time to establish’ factor.

So, what influences business value and what will people pay for?

It is possible to get a price that is widely different from the norm. Unique businesses, unique circumstances, and unique opportunities can

always produce ‘an out of the box’ price. If you can build something unique, then you may achieve a price beyond normal expectations. At the

end of the day however, the market will set the price.

If you are planning on selling your business, identify who your buyers might be. There could be a purchaser who is prepared to pay a large

premium to own your business because of the accretive value or because it is pivotal to their growth strategy.

And, even if you are not thinking about selling your business, the reality is that one day you will. If you build your business with this in

mind, then you should look to do the things that will grow your business value from year to year.

Our expert accounting and business consultants can help ensure a smooth transition when you're ready to step out from your business.

New Year’s Eve is famous for the New Year’s Resolutions people make to better themselves in the coming year. What about your financial future? How can you ensure you stick to your resolution?

Small business owners have a lot to think about: sales, staffing, customer service, vision, growth, the list goes on. In fact, it is hard not to think about your business when you’re a small business owner. Perhaps the one responsibility you would rather not think about is bookkeeping/accounting?

Some business owners try to avoid the hassles of accounting by simply ignoring the problem. “I’m too busy,” they say, but no business can hide from accounting. If late lodgement penalties aren’t motivating enough, hopefully the knowledge that you have basically no visibility into the vital indicators of business health will be.

Sure, there are online tools out there to make the process less burdensome, but could your time be better spent? And while you might think that a part-time bookkeeper might solve your problem, it really depends on your needs, and there are downsides there too.

HERE ARE what we think are THE TOP 5 REASONS TO OUTSOURCE YOUR bookkeeping to SMART Bookkeeping Solutions in Mornington

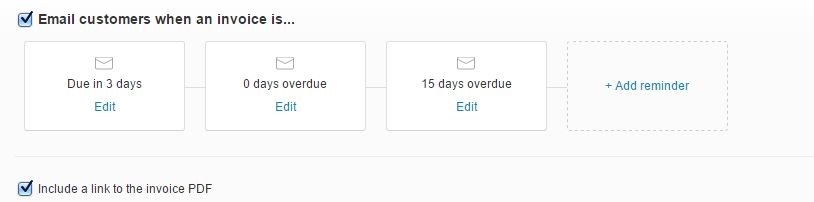

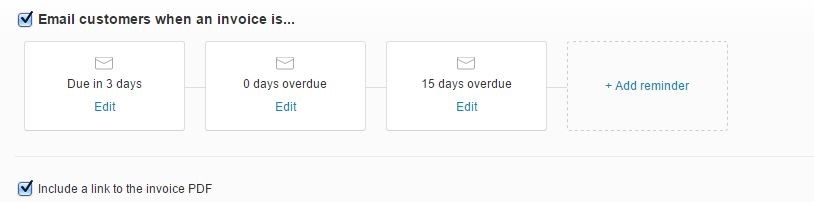

We often hear from clients “I often forget to send invoice reminders or statements and invoices are falling through the cracks, can Xero help with this?” Easy, of course it can!

It's time to celebrate! SMART Business Solutions are pleased to share with our clients some exciting news. The Finalists in the Australian Accounting Awards have been announced with the team being successful finalists in the following categories

- Best Marketing (you know we always try to be different!) Shannon was also interviewed http://www.accountantsdaily.com.au/breaking-news/8605-accountants-must-touch-their-clients-12-times-a-year

- Accounting Student - Well done Hayden!

- Office Administrator - Awesome effort Nicole!

- Partner of the Year - Shannon Smit for both Transfer Pricing Solutions & SMART Business Solutions

Quality Matters – Independent review with outstanding results for SMART Business Solutions

Paying an accountant to handle all of your financial reporting can be expensive, but if you have several different sources and deductions or if you own a small business, it can be worth it.

Is your business thriving, but you struggle to maintain positive cash flow?

Don’t let it crumble from underneath you

It’s nearly BAS time again - tips to make BAS processing easier

BAS time seems to come around quicker and quicker! Here are some tips to try and make it a little easier!

With June 30 quickly approaching we are pleased to provide our year end checklists and questionnaires to help you get organised.

For many business owners, superannuation is something that gets attention in June — when tax planning comes into focus. But the real opportunity lies in planning your super contributions at the start of the financial year, not the end.

The new financial year has officially clicked over – and with it comes the trio of mid-year obligations every employer needs on the radar: Single Touch Payroll (STP) finalisation, WorkCover declarations, and Payroll Tax annual reconciliation.

.jpg)